Hosted by Paul Cardarelli (JETNET) featuring experts Kevin Michaels (AeroDynamic Advisory), Richard Koe (WINGX), and Rollie Vincent (Rolland Vincent Associates/JETNET iQ)

Business aviation has long demonstrated resilience, continually adapting to shifting market conditions, regulatory changes, and geopolitical uncertainty. Over the past five years, that adaptability has been tested like never before—through COVID-19, fluctuating political landscapes, escalating trade tensions, and evolving government policies. Despite these challenges, the industry continues to adjust, seize new opportunities, and reinforce its dynamic nature.

In our recent webinar, “Turbulence Ahead? Navigating Tariffs, Trade, and Economic Uncertainty in Business Aviation,” experts Kevin Michaels, Richard Koe, and Rollie Vincent, hosted by Paul Cardarelli, examined the complexities of today’s economic environment. Supply chain disruptions, geopolitical instability, and policy shifts have created uncertainty, but the data presents a mixed picture.

Key Takeaways from the Webinar

- Preowned jet transactions rose 36.5% year-over-year, showing strong demand, especially for light and mid-cabin jets, even as values soften and aircraft take longer to sell.

- New aircraft deliveries are expected to grow 8% in 2025, with strong backlogs and production slots already sold.

- Fractional ownership is up 10% year-over-year, as more buyers explore flexible ownership options.

- Emerging markets like Brazil, Mexico, and the Middle East are becoming important growth areas as manufacturers expand beyond North America.

- The US business aviation market remains steady, with strong domestic demand helping to balance global uncertainty.

With those key takeaways in mind, let’s take a closer look at what the data and expert insights reveal about each of these trends—starting with what’s happening in the preowned market.

Transaction Volume Is Up—But So Are Concerns

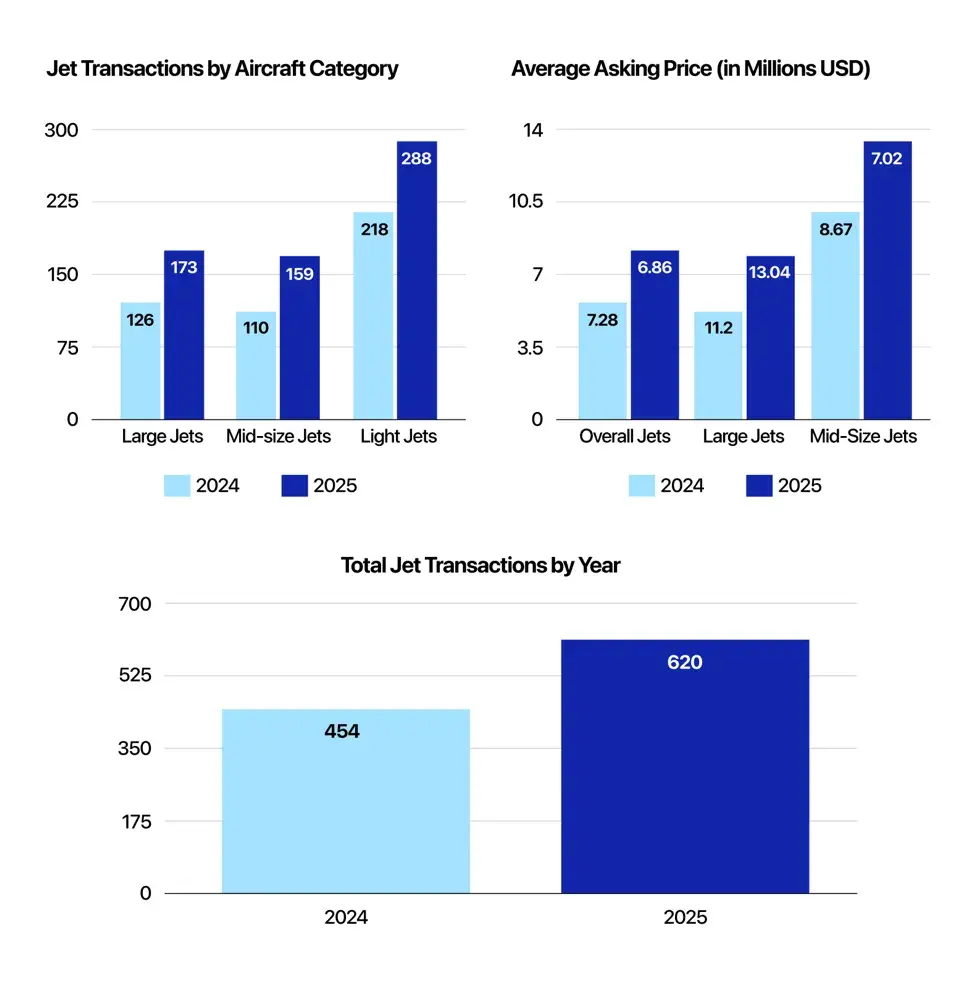

The pre-owned business jet sector is a key driver of business aviation, often serving as an early indicator of market trends. According to Rollie Vincent of JETNET iQ, transactions for pre-owned aircraft typically outpace new aircraft sales by a 4:1 ratio. Supporting this, JETNET’s Paul Cardarelli reports a 36.5% year-over-year increase in pre-owned business jet transactions in Q1 2025, signaling strong market activity. Notably, light jets saw an increase of 47 units, mid-cabin jets rose by 49 units, and large jets gained 32 units.

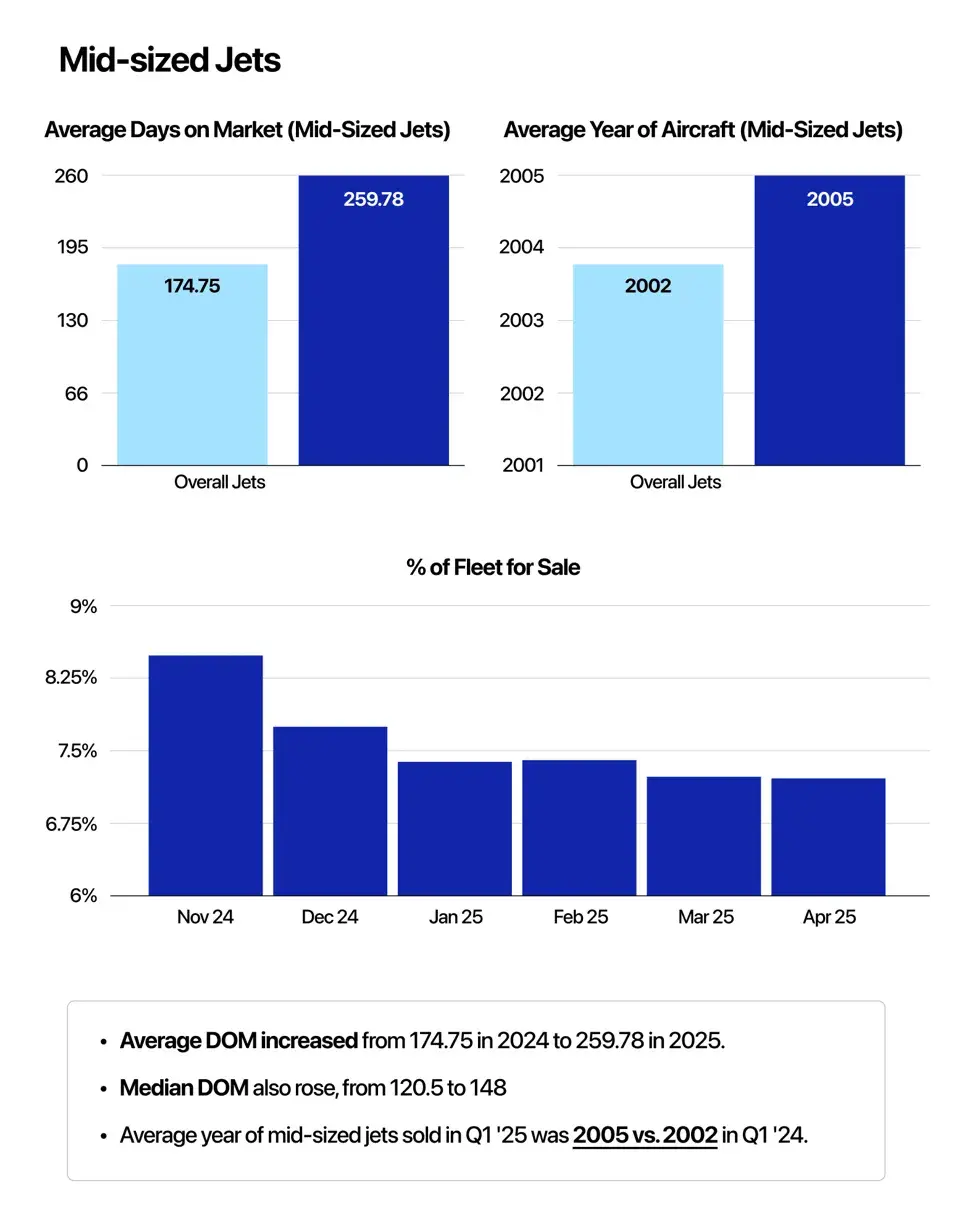

However, aircraft are remaining on the market for longer periods of time, with the average time to sell increasing by approximately 85 days compared to 2024. This slowdown in sales velocity reflects broader market trends, as pricing continues to soften across various segments, particularly in the mid-cabin category. Overall values have declined by 6.1%, with mid-cabin jets experiencing the steepest drop at 19%, despite newer aircraft entering the pre-owned segment (i.e., 20 years old vs. 22 years old previously). Light jets saw a moderate 5% price decline, while large jets defied the trend with a notable 16% price increase.

The extended listing durations and overall decline in aircraft values indicate that buyers may be approaching purchases more cautiously or shifting their focus toward alternative ownership models in response to evolving market conditions. Richard Koe of WINGX reports a steady rise in fractional ownership, with a 10% year-over-year increase, now reaching 91,000. Meanwhile, Cardarelli highlights that inventory remains tight, further shaping the landscape of business aviation transactions. Together, these factors underscore the changing dynamics of the market.

Shifting Gears: Transforming Uncertainty into a Launchpad for Growth in Emerging Markets

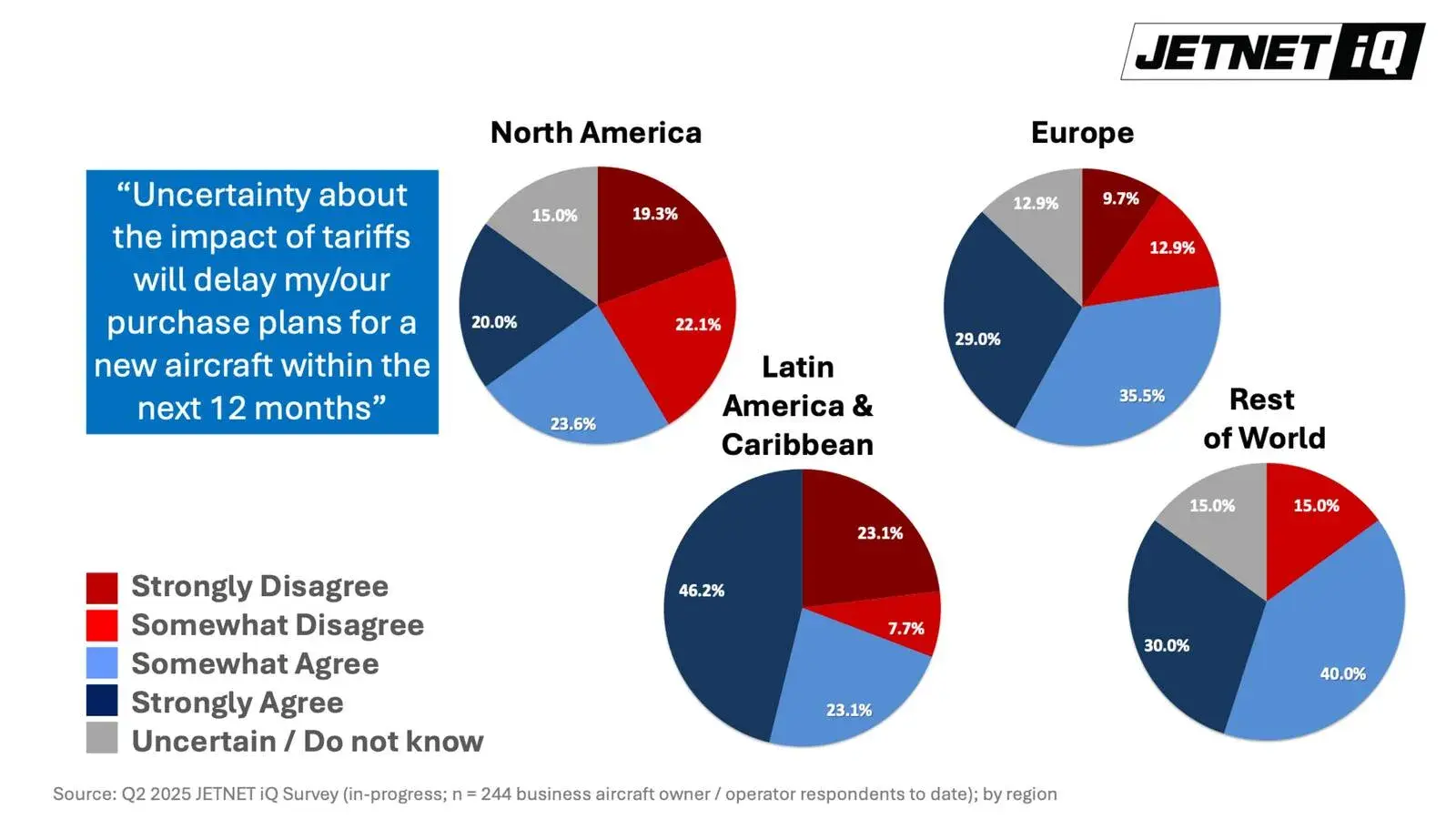

Given the evolving market conditions amongst the business aviation sector, it’s unsurprising that industry sentiment surveys reflect ongoing uncertainty. In fact, 53.3% of owners and operators believe the market has yet to reach its lowest point, signaling cautious optimism tempered by concerns about future stability. Rollie Vincent of Rolland Vincent Associates attributes this caution to concerns over economic growth, supply chain performance, and tariff-driven policy shifts. Latin America, Europe, and other global markets show the highest levels of concern, indicating potential demand drops for new aircraft over the next 12 months.

Still, Vincent maintains his forecast of 820 new business jet deliveries in 2025, an 8% increase over 2024. “The backlog is solid, production slots are sold, and the U.S. market remains dominant,” he said. “But uncertainty is quickly turning into unpredictability.”

He warns that tariffs could reshape global demand, pushing OEMs to expand beyond North America. As U.S. GDP growth slows, markets such as Brazil, Mexico, and the Middle East may gain greater significance. Non-U.S. markets that house younger, larger, and longer-range fleets present attractive opportunities for manufacturers. Brazil and Mexico, for example, despite being two of the largest business aviation markets outside the U.S., often receive less attention than they deserve. Meanwhile, business aviation is expanding rapidly in the Middle East, particularly in the UAE and Turkey, as these regions continue to embrace private aviation.

While transaction activity remains strong, shifting demand patterns highlight the need for OEMs to rethink their global strategies amid an evolving economic and geopolitical landscape.

Tariffs, Geopolitics, and Supply Chains: The Elephant on the Tarmac

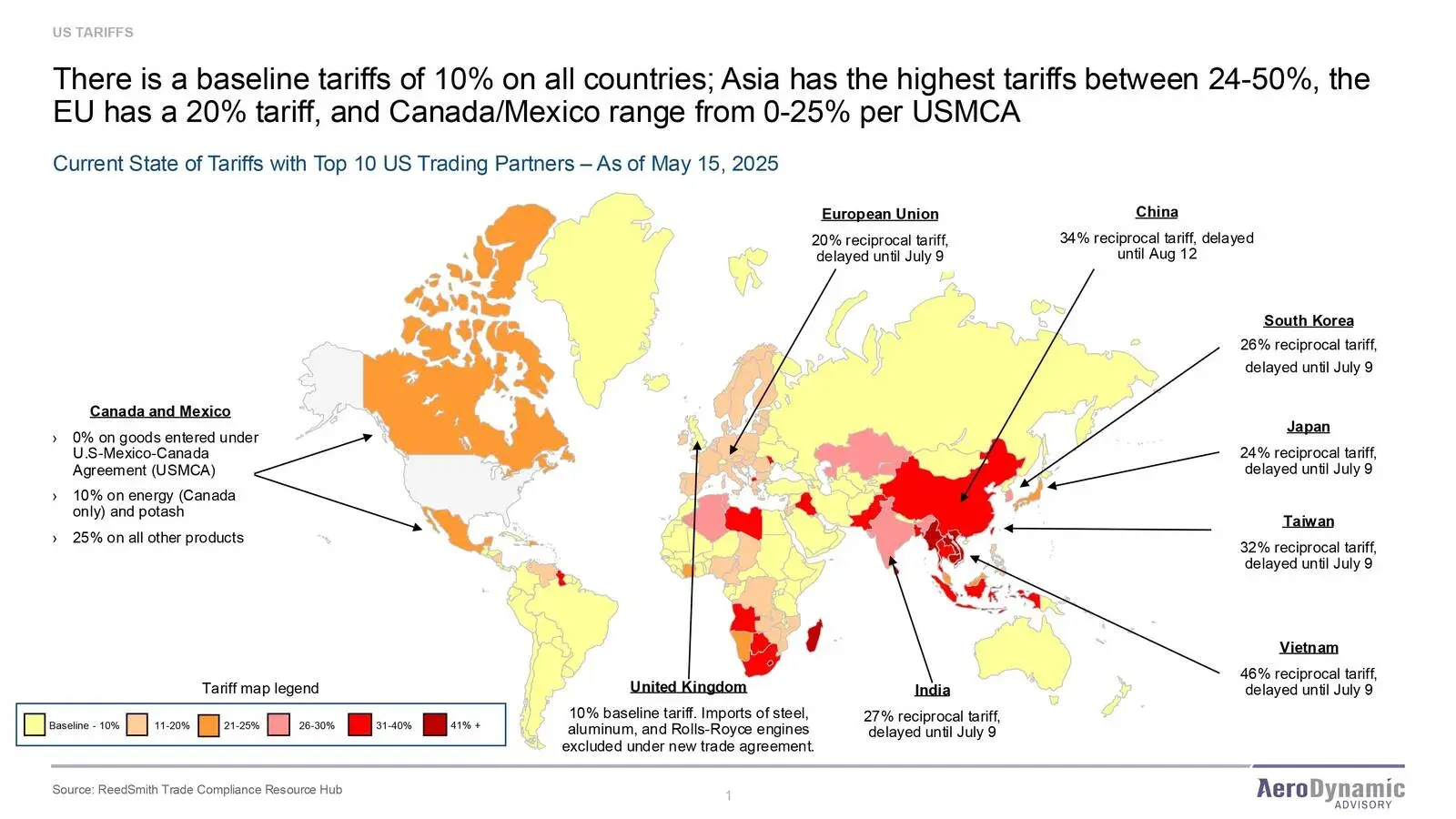

With the U.S. administration set to introduce new policies reshaping global tariffs and trade agreements on July 9, 2025—dubbed “Trump Tariff Liberation Day”—concerns are rising over its impact on transatlantic trade. The reinstatement of a 50% tariff on EU aircraft threatens to disrupt deliveries, forcing OEMs and buyers to reconsider and adapt their purchasing strategies.

Kevin Michaels of AeroDynamic Advisory warns that these tariffs could fragment supply chains, create inefficiencies in regional distribution, and drive up maintenance, repair, and overhaul (MRO) costs. “We could see the aftermarket shift from global to regional hubs just to avoid punitive tariffs,” he noted. Already, the once-fluid movement of aircraft parts has slowed, increasing uncertainty for distributors managing global inventories. If tariffs persist, Michaels warns that supply chains may shift from centralized distribution models to regionalized strategies, leading to reduced efficiency and higher costs.

Compounding these challenges, business aviation has faced substantial price inflation, with spare parts and maintenance costs rising by 8–10% in recent years. OEMs are expected to increase aftermarket prices further to offset tariff impacts, extending inflationary pressure across the sector. Meanwhile, overall demand may decline, particularly as corporations scale back business travel amid growing economic uncertainty.

At the same time, aerospace supply chains are grappling with several major bottlenecks:

- Aero Engine production remains constrained, particularly in rotating parts and castings, as OEMs focus more on aftermarket revenues rather than ramping up new production. Airbus and Safran continue to clash publicly over output levels, with Airbus pushing for higher rates while Safran benefits financially from limiting supply.

- Aircraft Interiors are facing growing difficulties, affecting both business aviation and commercial transport. Profitability issues among Tier 1 suppliers, coupled with certification bottlenecks at EASA, where only two inspectors manage approvals, have further delayed progress.

- Small and Mid-Sized Aerospace Suppliers in North America and Europe are also struggling with capital shortages, limiting their ability to scale production, while hiring difficulties continue to stall growth across the sector.

Adding to these concerns is the ongoing titanium supply chain issue. Prior to Russia’s invasion of Ukraine, Russian supplier VSMPO-AVISMA provided 40–45% of global aerospace titanium. This supply included Rotating grade, used in aero engines, including disks and other key components and Structural grade, used in aerostructures, landing gear, and various aircraft parts. Since the invasion, North American aerospace companies have largely moved away from Russian titanium sources. However, Airbus, Safran, and Rolls-Royce remain heavily reliant on Russian titanium and have lobbied against EU sanctions, citing difficulties in securing alternative supply. While new titanium mills in the U.S. (Timeet and ATI) aim to reduce dependency on Russian imports, supply chain vulnerabilities persist. If Russia halts titanium exports, critical parts of the industry could face disruption.

As the global aerospace industry navigates mounting uncertainties, the interplay of tariffs, supply chain bottlenecks, and geopolitical shifts will determine its trajectory in the coming months. OEMs and suppliers are being forced to rethink their strategies, balancing cost pressures, regional trade dynamics, and evolving regulatory landscapes. While localized production efforts may help mitigate some risks, the continued strain on engines, interiors, and raw materials, particularly titanium, remains a formidable challenge. As businesses brace for the impact of shifting trade policies, adaptability and strategic foresight will be crucial in ensuring long-term resilience and sustained growth.

Global Flight Trends: A Mixed Picture

Although a market slowdown was widely anticipated following President Trump’s tariff announcement in early April, Richard Koe of WINGX reports that global business jet flights experienced a modest 1.4% increase compared to previous weeks, defying expectations. However, he notes that year-over-year growth has slightly tapered (3.3% vs. 3.4%), with notable regional disparities:

- U.S. & Canada: Cross-border business jet activity fell 4% year-over-year, likely influenced by shifting travel plans and concerns over tariffs. However, the U.S. business aviation market remains dominant, with only 7% of its business jet flights classified as international. This robust domestic demand provides stability, helping to shield the sector from some of the volatility affecting global markets.

- Germany: Flight activity declined 8% year-over-year, with 2025 levels trailing even pre-pandemic 2019 figures. This continued slowdown is linked to trade disruptions, energy transition challenges, and Net Zero policies, which have intensified post-tariffs.

- Europe & Asia: Both regions remain sluggish, with business jet activity just 2–3% higher than in 2019—far behind U.S. growth. However, new U.S. trade agreements in the Middle East, particularly Saudi Arabia, could stimulate demand and create new growth opportunities.

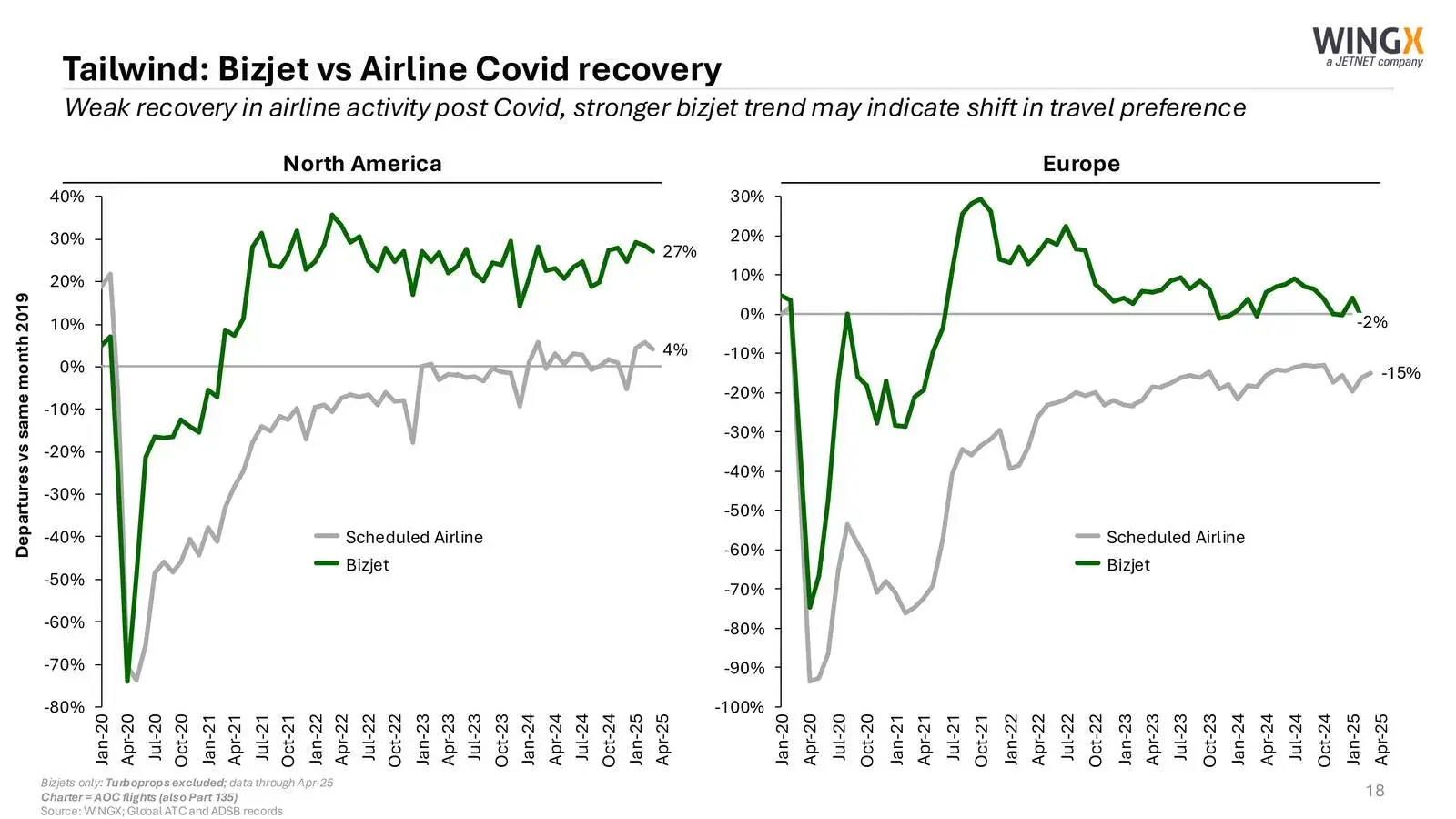

Meanwhile, corporate flight departments have maintained a three-year decline, a trend that continues post-tariff announcement. Part 135 charter activity is also softening, as companies and private travelers are possibly turning to commercial airlines instead. This transition is occurring despite business aviation rebounding far more robustly from the COVID-19 pandemic than commercial airlines, particularly in North America and Europe.

While U.S. airline traffic has finally surpassed 2019 levels, European carriers continue to lag behind significantly. Compounding these challenges, commercial airline connectivity has deteriorated, with unique city-to-city connections in both the U.S. and Europe remaining depleted compared to pre-pandemic levels. Premium cabin availability has also declined, and persistent delays and cancellations have pushed more travelers toward private aviation as a more reliable alternative. Given these circumstances, the slowdown in Part 135 charter activity stands out as an unexpected trend.

Meanwhile, business jet flight sectors in North America have surged by 27% compared to 2019, demonstrating sustained growth that has yet to be mirrored in Europe. Much of this expansion can be attributed to the increasing inconvenience of commercial airline travel, which has reinforced business aviation’s appeal as a flexible and efficient solution for travelers navigating evolving market conditions.

While the civil aviation industry continues to face challenges, shifting demand patterns and strategic market adaptations underscore the evolving landscape of business aviation, where adaptability will be essential for capitalizing on emerging opportunities.

Looking Ahead: Navigating the Next 12 Months

- Continued Transaction Activity: Despite softening values and longer sales cycles, the pre-owned market is expected to remain active, particularly in light and large jet segments.

- Steady New Aircraft Deliveries: Deliveries are projected to increase by 8% in 2025, supported by solid backlogs and strong demand in the US.

- Cautious Buyer Sentiment: Over half of operators believe the market has not yet hit bottom, suggesting conservative spending and slower decision-making in the near term.

- Global Shift in Demand: Growth is likely to come from non-US regions like Brazil, Mexico, and the Middle East, as OEMs look to diversify amid geopolitical and tariff pressures.

- Tariff and Supply Chain Disruptions: The July 2025 trade policy changes could cause pricing volatility, regionalize supply chains, and pressure MRO and parts costs—especially in Europe.

- Opportunities in Flexibility: With fractional ownership and alternative models on the rise, operators and providers who can offer adaptable solutions will be better positioned to capture demand.

Enjoyed this webinar and the insights shared? If you’re looking for more, don’t miss the JETNET iQ Summit this September in Washington, D.C., where business aviation’s top leaders come together to exchange ideas. This event offers a unique opportunity for industry professionals to engage in forward-thinking discussions, explore market strategies, and anticipate key developments shaping the future. As business aviation continues to evolve, collaboration, innovation, and adaptability will be essential in driving a more stable and sustainable industry.