After several years of post-pandemic expansion, business aviation is entering a new chapter, one marked by resilience, recalibration, and precision. At NBAA-BACE 2025, JETNET iQ and WINGX presented fresh intelligence revealing that the market isn’t slowing down, but rather refining itself for the decade ahead. The data was unveiled during the Media Day Press Conference, “Charting the Course: Strategic Forecasts & Market Intelligence,” held on Monday, October 13, 2025, at the Las Vegas Convention Center’s West Hall (Room W209), led by Rolland Vincent of JETNET iQ and Christoph Kohler of WINGX. Together, these two industry intelligence leaders painted a clear picture of a sector that continues to grow, even as it adapts to shifting economic, operational, and policy dynamics.

From Recovery to Refinement

|

|

According to JETNET iQ, the global business aviation market has moved past its rebound phase into a more deliberate, measured trajectory. Economic growth has softened across major regions, yet demand for private flying remains robust. Persistent challenges such as tariffs, supply chain bottlenecks, and labor shortages still shape operations, but they haven’t stalled progress.

JETNET iQ forecasts 820 new business jets to be delivered in 2025, an 8% year-over-year increase, along with 365 turboprops, down 5%. The first half of the year saw 354 jets delivered, up 10% from 2024. The “Big Five” OEMs (Bombardier, Dassault, Embraer, Gulfstream, and Textron Aviation) collectively hold a $55.5 billion backlog, representing more than two years of production at current build rates.

This steady pace of manufacturing mirrors what WINGX is seeing in the skies: 4.5 million business jet and turboprop flights through September 2025, a 3.7% increase compared to the same period last year. Together, both datasets underscore an important theme that the industry’s growth engine is still running strong, just at a more sustainable speed.

The Center of Gravity Shifts — But North America Still Leads

|

|

Where those flights are taking place also tells a story. WINGX data shows that North America remains the core of global business aviation, accounting for roughly two-thirds of all activity, with departures up 4% year-to-date. Florida and Texas continue to anchor the market, driven by wealth migration and corporate relocations from higher-tax regions.

Domestic operations still account for 87% of all U.S. business jet flights, with most missions under 1,000 nautical miles, reinforcing business aviation’s role as a short-range connector of people, capital, and opportunity.

By contrast, Europe’s recovery has flattened, with flight activity growing just 1% annually since 2019, according to WINGX. Geopolitical pressures, environmental regulation, and slower economic expansion have cooled demand. Yet, emerging markets are taking flight. India’s active business jet fleet has now surpassed China’s, and the Middle East continues to expand rapidly, a clear sign that the next phase of growth may come from outside traditional markets.

Confidence, Policy, and the Power of Clarity

{kind=link}

While regional performance varies, JETNET iQ’s Q3 2025 Global Business Aviation Survey reveals a remarkably stable level of industry confidence. 55% of respondents described current market conditions as favorable, 31% said the market is near a low point, and only 14% believe it’s at one. A balance that reflects cautious optimism.

That optimism is grounded in performance. 91% of business aircraft operators told JETNET iQ that their companies are more profitable because of business aviation, highlighting its role as a strategic business asset.

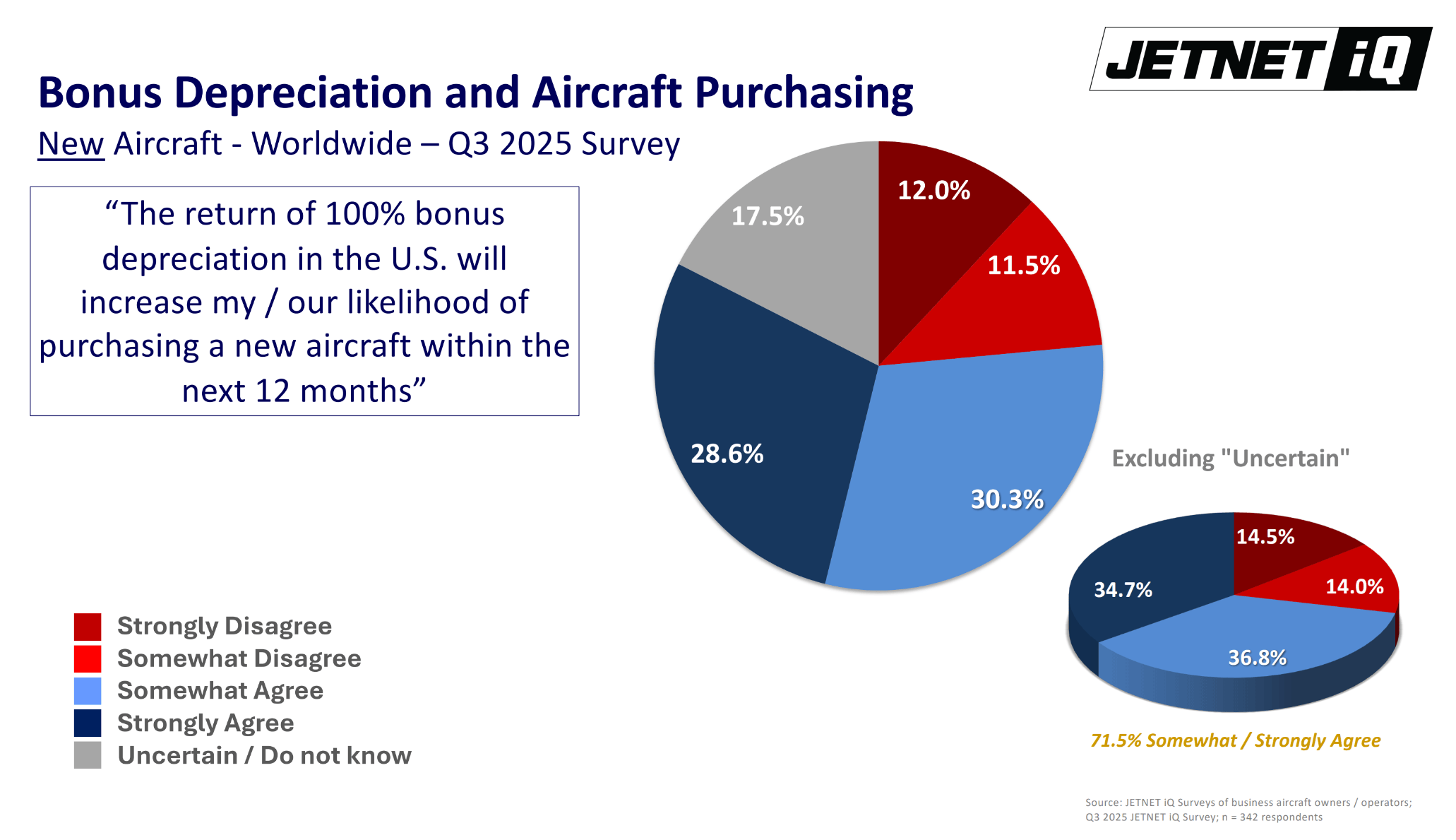

Policy clarity, however, remains a key catalyst for fleet renewal. JETNET iQ found that over 70% of respondents would be more likely to purchase a new aircraft if the U.S. reinstated 100% bonus depreciation, while 56% said tariff uncertainty could delay those decisions. The takeaway: fiscal stability directly drives confidence and capital flow into the market.

Market Structure: Scale Wins, Strategy Matters

|

|

Both data sets point to a market where scale and strategy are shaping the competitive landscape. WINGX reports that large operators like NetJets, Flexjet, flyExclusive, and Wheels Up, now control three-quarters of all North American charter and fractional flight hours, up 16 points since 2019. Smaller charter companies are ceding ground as fractional programs expand, fueled by new entrants and double-digit year-over-year utilization growth.

However, both WINGX and JETNET iQ data suggests this growth is not purely additive. Some of the activity in the fractional and management space appears to be substituting for traditional corporate flight department flying, rather than expanding the total market. The result is an industry reshaping its business model around flexibility, utilization efficiency, and shared access rather than simply adding more aircraft.

Aircraft Trends and OEM Performance

|

|

Both datasets align on one theme: the move toward larger, longer-range aircraft. WINGX notes that super midsize and ultra-long-range jets now account for a disproportionate share of global departures, reflecting growing demand for productivity and reach.

JETNET iQ’s buyer data confirms the same preference. On the new aircraft side, the Gulfstream G400, G700, and G800, Bombardier Challenger 3500, Dassault Falcon 6X, and Embraer Phenom 300 lead global demand. In the pre-owned market, proven performers such as the Citation XLS+, Phenom 300, Falcon 2000/900, and King Air 260 remain among the most sought after.

OEM utilization trends, according to WINGX, show Bombardier and Embraer leading flight activity growth in 2025, contributing heavily to the 83% market share held by the top five manufacturers (Bombardier, Gulfstream, Embraer, Cessna, and Hawker Beechcraft). On the turboprop side, Pilatus continues its steady ascent, increasing its share from 24% in 2019 to 29% in 2025.

The Decade Ahead: Data-Driven Discipline

|

|

Looking forward, JETNET iQ projects 9,700 new business jets worth $335 billion to be delivered through 2034, alongside 4,100 turboprops valued at $24 billion.

- Ultra-long-range jets will represent 22.5% of deliveries,

- Super midsize jets 17.1%, and

- Light jets 19.5%.

As the industry balances growth with sustainability, leaders expect to navigate supply chain recovery, workforce challenges, MRO capacity limits, and decarbonization goals. Yet opportunity abounds. Respondents to JETNET iQ’s survey identified the MRO sector as the most attractive near-term investment opportunity, followed by hybrid turbine and SAF technologies, fractional models, and electric propulsion development.

WINGX echoes that cautious optimism. Its 2025 outlook anticipates continued, if moderate, growth over the next 12–24 months, supported by wealth creation, limited airline capacity, and expanding user adoption—powerful tailwinds that continue to outweigh macroeconomic turbulence.

The Bottom Line

Together, JETNET iQ and WINGX reveal a business aviation industry that is evolving, not retreating. It is refining, not rebounding. The fundamentals remain strong: demand is stable, utilization is growing, and both manufacturing and operations are guided by data-backed precision.

As Rollie Vincent of JETNET iQ summarized, “Business aviation is no longer in recovery mode—it’s entering an era of strategic precision.” 2025 stands as its proof: a market guided by intelligence, discipline, and deliberate progress, and an industry not chasing altitude, but mastering stability at cruising speed.

Subscribe to WINGX Weekly Bulletin for more insights.

Learn more about JETNET iQ.