JETNET iQ PULSE

Issue 51 – From Both Sides Now

Table of Contents

From Both Sides Now

Canadian phenom Joni Mitchell burst onto the folk scene in 1966‑67 with Both Sides Now, a breakout hit about clouds, love, and life. An 11‑time Grammy winner, she also has an aviation connection dating back to her childhood on RCAF bases, where her father trained WWII pilots. Both Sides Now has since been covered by more than 1,000 artists.

As analysts of the business‑aviation industry, we’ve learned that compelling research starts with curiosity and good questions, leading to insights grounded in evidence from multiple sources. Asking not only “What could this mean?” but also “What else could this mean?” drives deeper analysis and alternative interpretations.

Since 2011 our JETNET iQ Surveys have reached owners and operators in 140+ countries. With 27,000+ responses, these surveys transform trusted data streams into actionable intelligence—the secret sauce we bring to the table.

In this issue we delve into trade tariffs—now a preferred negotiating tool of the U.S. administration. Broad‑based tariffs are a blunt economic instrument with far‑reaching, often unintended consequences. Yet civil‑aircraft manufacturing remains globally integrated and largely U.S.‑centred, thriving for 45+ years under the tariff‑free Agreement on Trade in Civil Aircraft (ATCA). In short: free trade works, no matter which side of the table you sit on.

“Free trade works, no matter which side of the table you sit on.”

Rollie Vincent

JETNET iQ Creator/Director

Outlook

Business‑Jet Unit Deliveries & 2025 Forecast

Forecasting in an industry as globe-spanning, technologically complicated, and rules-based as international civil aviation and aerospace is highly specialized and surely not for the faint of heart. As much art as science, the vital details of forecasting methodologies are familiar to few, practiced well by even fewer, and lost on many. While many forecasts begin with a math equation, that is typically an initial step in the process for more experienced prognosticators, seasoned by knowledge gained in rooms around the industry where strategic decisions are made.

In our years of analyzing markets and understanding human behaviors, forecasting in today’s business aviation environment seems uniquely different. During our still- nascent 21st Century, business aviation has already endured the 9/11 terrorist attacks, devastating regional wars, the Global Financial Crisis, and COVID-19. Chaotic weather patterns, ceaseless geopolitical conflicts, and tariff wars are the latest Black Swan events in our daily dose of breaking news headlines. While the economic impacts of the U.S. Administration’s focus on tariffs are unknown, policy uncertainty and unpredictability is already causing concern amongst investors, business leaders, and consumers, which is already in evidence with slower growth, higher prices, and delayed purchasing. In business aviation, the near-term outlook for new aircraft deliveries has been largely set in place for some time. Long-ago placed orders for aircraft are buried in OEM backlogs at historically high prices, shielding for now these organizations for the most part from a downturn in demand for the time being. How this plays out as order backlogs are drawn down is something to watch closely. Our near-term forecast is for ~10% higher business jet deliveries in 2025 YoY, representing the industry’s highest unit output since 2009.

Business Jet Unit Deliveries and JETNET iQ Forecast for 2025 Year-End

Sources: Company reports; GAMA (historical); JETNET iQ (forecast)

Business Conditions (July 2025)

GDP The Economist’s GDP growth forecasts (Jul. 10, 2025) for 2025 are: U.S. +0.9%, Euro Area +1.2%, U.K. +1.0%, Mexico -0.2%, Brazil +2.2%, Canada +1.0%, China +4.7%, Australia +1.7%, and Russia +0.9%

Business jet cycles (take-offs and landings) for Jan.-Jun. 2025 were down 13.8% YoY for U.S. Part 91, up 11.1% YoY for U.S. Part 91K, up 8.0% YoY for U.S. Part 135, and up 0.7% YoY for European operations

Dow Jones Index (U.S.) was up 9.5%,

FTSE 100 (U.K.) was up 9.5%,

CAC 40 (France) was up 2.5%, and

DAX 30 (Germany) was up 29.9%

YoY on Jul. 15, 2025

U.S. Index of Consumer Sentiment was 60.7 in Jun. 2025 vs. 52.2 in May 2025 and 68.2 in Jun. 2024 YoY; Euro Area Economic Sentiment Indicator was 94.0 in Jun. 2025 vs. 94.8 in May. 2025 and 96.0 in Jun. 2024 YoY

U.S. unemployment rate (seasonally adjusted) was 4.1% in Jun. 2025 representing 7.0 million unemployed people, compared to 4.1% in Jun. 2024

U.S. Purchasing Manager Index (Manufacturing PMI) was 49.0 in Jun. 2025, up from 48.5 in May 2025 and from 48.3 in Jun. 2024; Euro Area Business Climate Indicator was -0.78 in Jun. 2025, down from -0.57 in May 2025 and from -0.48 in Jun. 2024

Transactions of pre-owned business aircraft in the first 4 months of 2025 were 824 jets and 381 turboprops, up 24.7% and up 3.3% respectively YoY (JETNET as of May 1, 2025; whole retail transactions only)

Business aircraft deliveries registered YTD in 2025 are 341 jets (including Cirrus and Boeing / Airbus single-aisle) and 135 turboprops (Source: JETNET – as of Jul. 15, 2025)

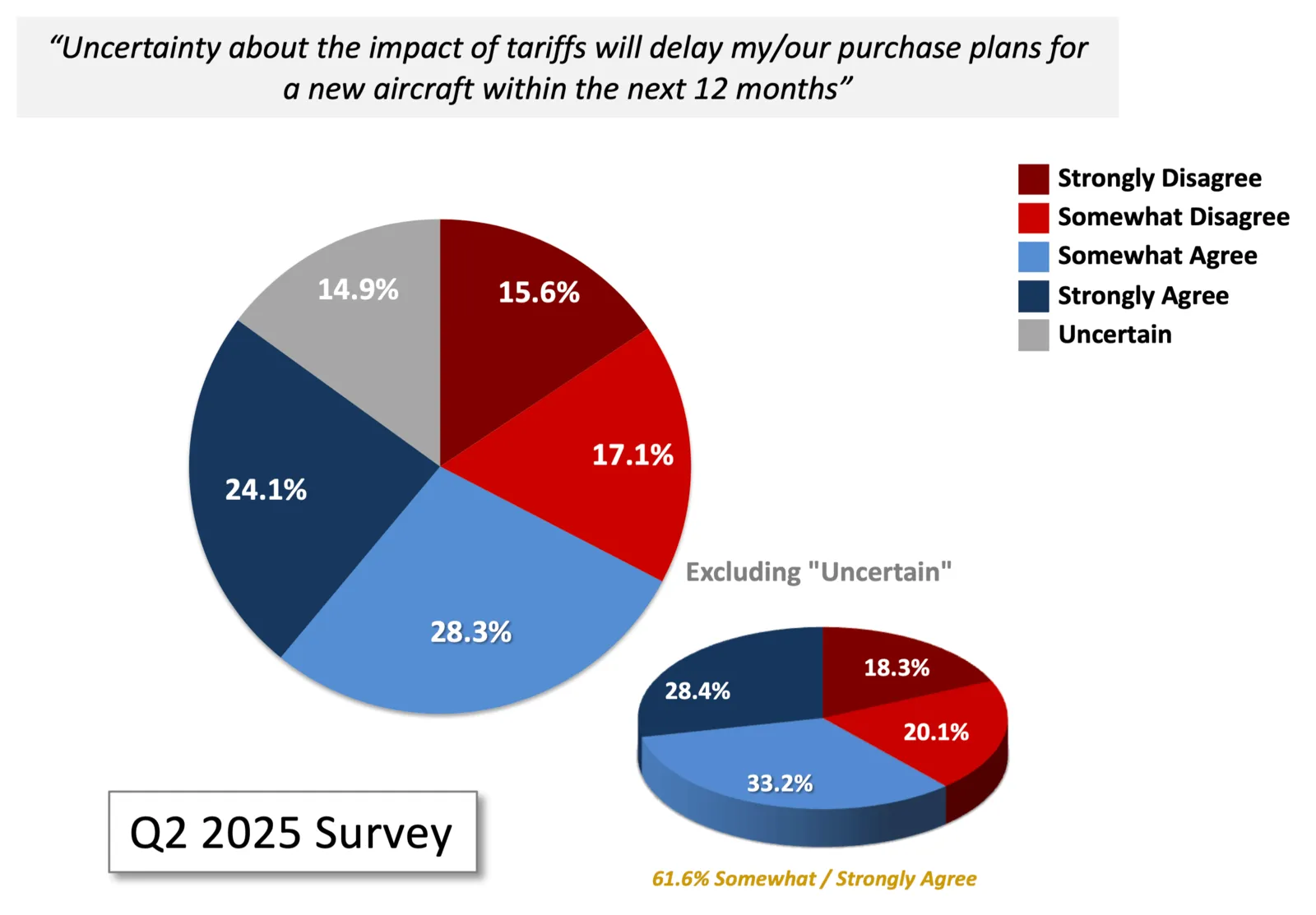

Q2 2025 JETNET iQ Survey: Tariff Impacts on Aircraft Purchases

Business aircraft owners / operators who responded to our Q2 2025 JETNET iQ Survey expressed considerable concern about tariff-related uncertainties with regards to their new aircraft purchase plans over the next 12 months. Almost 62% of respondents with an opinion agreed that uncertainties about the impacts of tariffs would delay their new aircraft purchase plans. While most OEMs have strong backlogs representing 1.5-2 years of production, insights like these will hopefully compel policymakers to sit up and take notice. Business aviation has thrived for 45+ years in what has been an essentially tariff-free international trading environment which has served stakeholders very well. Through the first half of 2025, uncertainty and unpredictability appear to have become the norm rather than the exception for many business aircraft customers and their organizations.

Impact of Tariffs on New Aircraft Purchase Plans

Worldwide - Q2 2025 JETNET iQ Survey

Source: Q2 2025 JETNET iQ Survey (n= 360 owner / operator respondents from 48 countries)

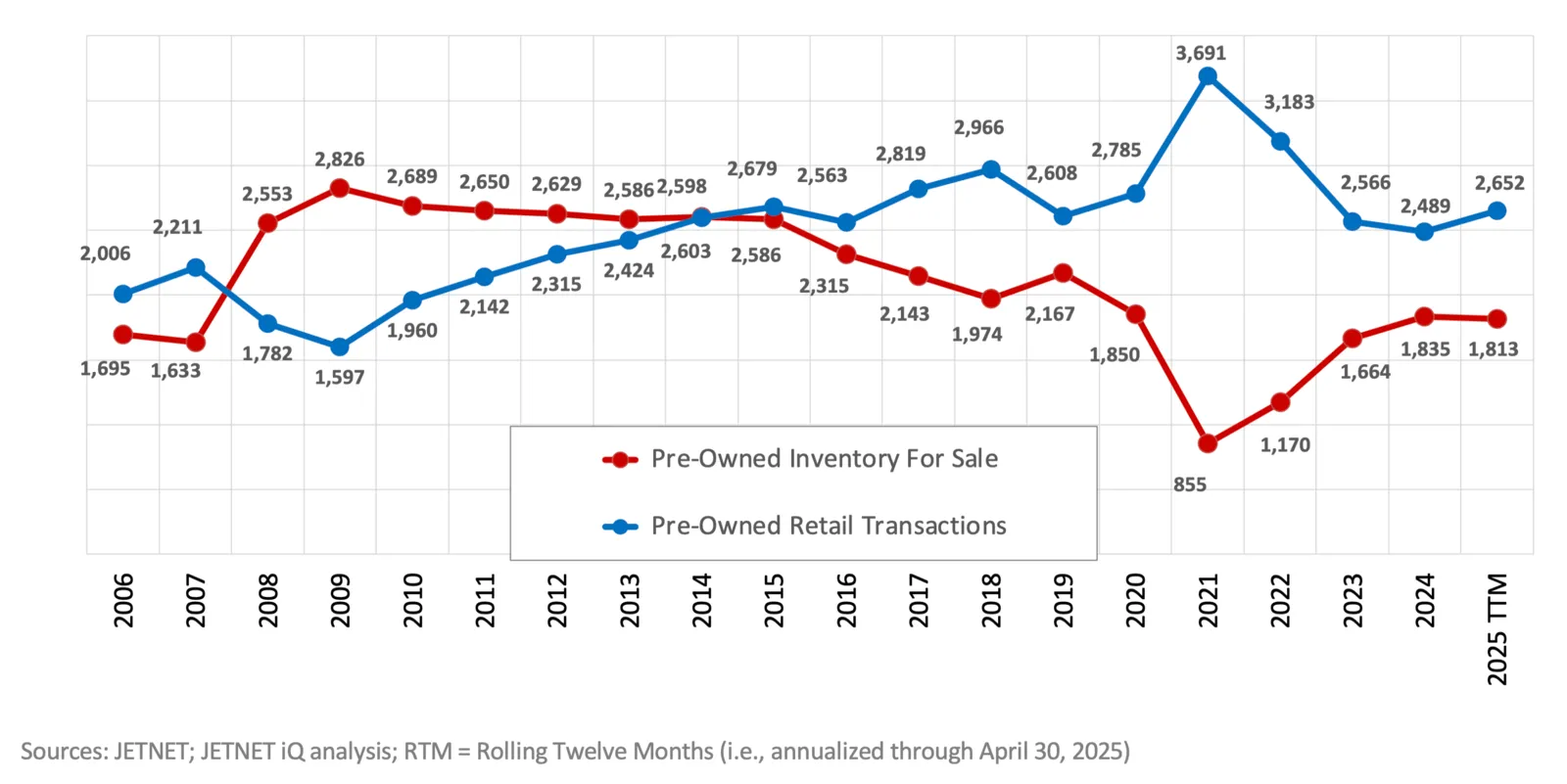

Pre-Owned Business Jet Transactions and Inventory

The pre-owned business jet marketplace continues to rebalance following unprecedented demand in 2021 through mid-2022 in the immediate aftermath of COVID-19. There were 824 retail pre-owned jet transactions (whole aircraft only) in the first 4 months of 2025 according to JETNET records, up an impressive 24.7% YoY and a fast start to the new year. The return of 100% bonus depreciation in the U.S. is widely anticipated to provide further lift to business aircraft sales, especially in the 2nd half of 2025. In the full year 2024, retail pre-owned jet transactions were down ~3% YoY while year-end inventory was up ~10% versus where it finished 2023.

As usual, the most attractive inventory of young, pedigreed models remains in short supply, with virtually no availability in some cases depending on the model and vintage of greatest interest to the buyer. JETNET databases indicate that there were 145 business jets delivered new since the beginning of 2020 that were listed as for sale in mid-July 2025, representing just 0.6% of the in-service fleet worldwide. In the popular Super Mid-Size Jet segment, just 7 aircraft that delivered new since the beginning of 2020 were listed as for-sale in mid-July 2025, including not a single example of the segment-leading Challenger 350 / 3500.

Sources: JETNET; JETNET iQ analysis; RTM = Rolling Twelve Months (i.e., annualized through April 30, 2025)

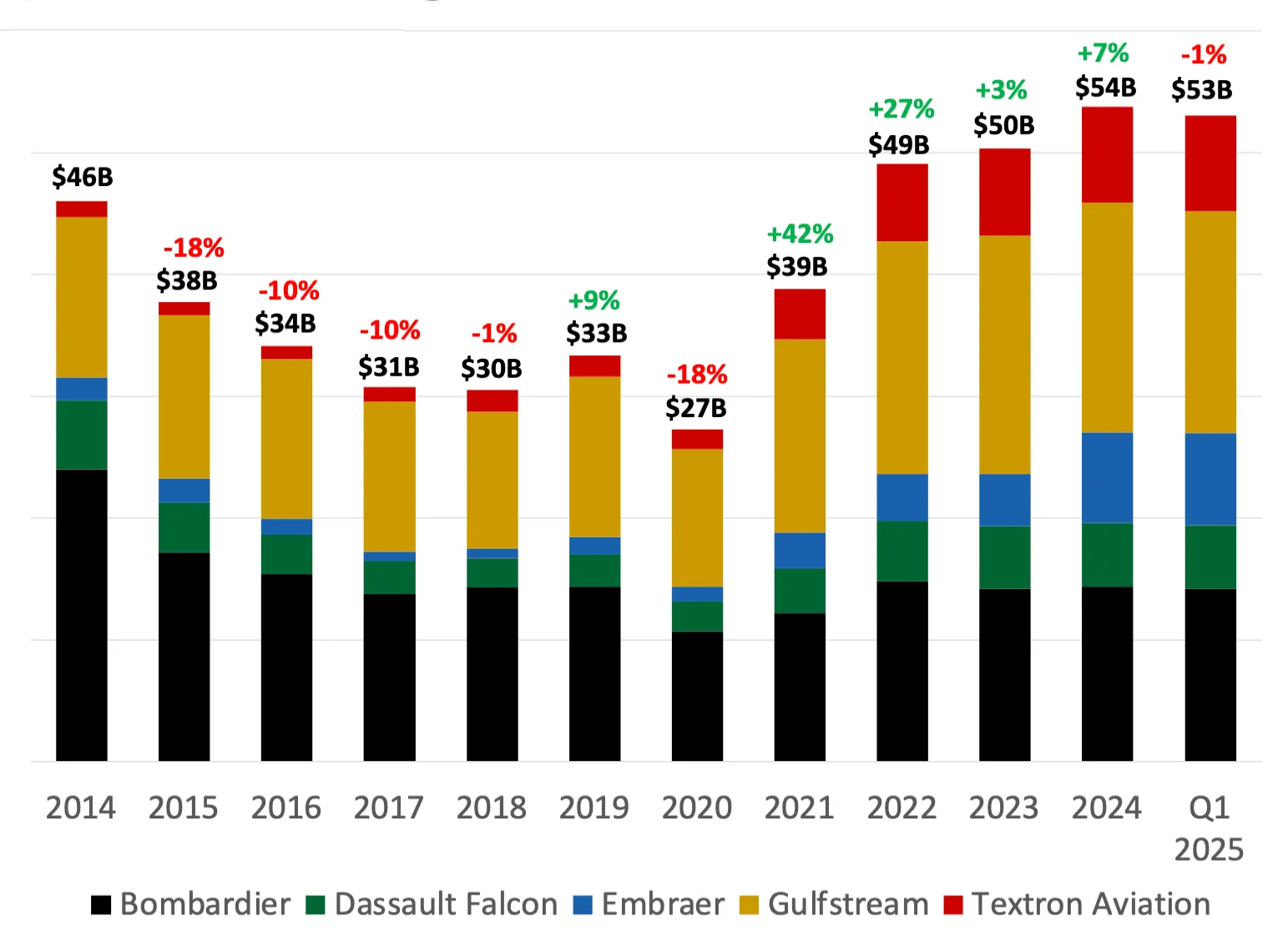

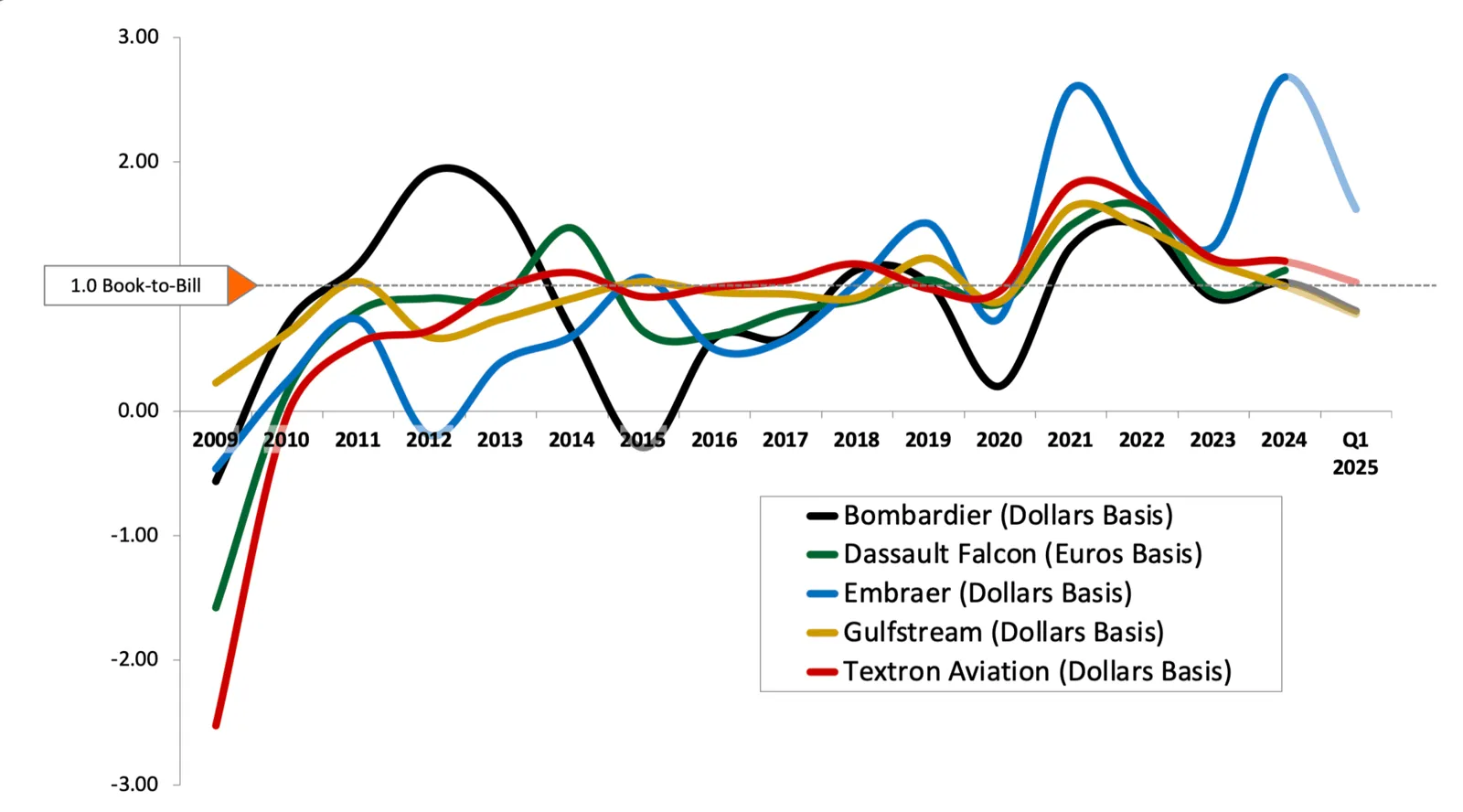

OEM Order Backlogs & Book‑to‑Bills

Total order backlog value at the 5 largest business aircraft manufacturers has remain relatively stable for the last 2-3 years near $53-54B, representing 18-24 months of production at recent rates. While book-to-bill performance has downshifted from (frankly) unsustainable levels in 2021 and into 2022, efforts to accelerate production continue to be constrained by supply chain bottlenecks (albeit at fewer suppliers) and lingering staffing challenges in an historically tight labor market. New aircraft prices have reportedly now begun to come back from their recent near-stratospheric levels, as demand signals are complicated by tariff and broader macroeconomic uncertainty and unpredictability.

“Big 5” Business Aircraft OEM Backlogs

$U.S. in Billions - Through Q1 2025

“Big 5” Business Aircraft Book-to-Bills

Through Q1 2025

Source: Company reports; JETNET iQ analysis and estimates

About JETNET iQ

JETNET iQ is a market research, strategy, and forecasting service for business aviation with 3 main elements:

- JETNET iQ Reports are the definitive analytical reference for business aviation, incorporating quarterly state-of- the-industry analyses, aircraft owner / operator surveys, and detailed aircraft delivery and fleet forecasts.

- JETNET iQ Summits are unique conferences providing industry insights, thought leadership, and networking opportunities with titans of the industry.

- JETNET iQ Advisory services include bespoke research, analytics, insights, forecasts, and recommendations for clients on strategic topics including market intelligence and next-generation products and services.

JETNET iQ’s proprietary quarterly surveys of the worldwide community of business aircraft owners and operators are carefully designed to generate statistically sound data that gauge customer sentiment, brand perceptions, aircraft purchase / selling / utilization expectations, and areas of topical interest in a fast-changing marketplace. JETNET iQ Surveys are password-protected and by invitation-only to ensure superior quality. Survey respondents include both aviation professionals and senior management and closely reflect the worldwide distribution of the business jet and turboprop community. Since Q1 2011, more than 27,000 respondents from 140+ countries and territories have participated in JETNET iQ Global Business Aviation Surveys, generating the largest commercially available database of its kind in the world.

JETNET iQ, a respected source of industry intelligence and voices-of-the customer research, is a result of a long- term partnership between Rolland Vincent Associates (RVA) and JETNET. RVA is an advisory service specializing in business aviation industry analytics, market and competitive intelligence, and forecasts that support leadership decision-making. Established in 1988, JETNET powers investment, growth, operations, and safety through the most comprehensive data and actionable intelligence in aviation worldwide.

For more information on JETNET iQ, please contact:

Rolland Vincent, JETNET iQ Creator/Director

Tel: 1-972-439-2069

e-mail: rollie@jetnet.com

Material in this publication may not be reproduced, stored in a retrieval system, or transmitted in any form or by any means (electronic, mechanical, photocopying, recording, or otherwise) without the prior written permission of the publisher.

Unlock the Power of WINGX Global Insight

From operators to investors, gain actionable intelligence tailored to your needs for the most comprehensive analysis of global flight trends.

Take A

Test Flight

Get a personalized demonstration of the world’s premier aviation intelligence platform.